Insurance is making its way into nature market - a sign that the sector is growing up?

How does the nature markets sector deal with and mitigate risk as it grows up?

Last week I found myself spontaneously spending an afternoon at a forum on insurance in nature markets, hosted by the Scottish Forum for Natural Capital, right around the corner from where I live. It turned out to be an excellent few hours, with some of the well-known figures in the Scottish natural capital scene, including Eleanor M Harris and Dr Hannah Rudman, and representative of key actors in the sector. The title was “Insuring Nature Restoration: Carbon, Biodiversity and Beyond” and I went in genuinely curious.

Insurance is one of those subjects that people in nature markets are increasingly intrigued by but do not yet know quite enough about, myself included. Coming out of the afternoon, I felt it deserves a proper explanation, because it could well be one of those markers that signals a market moving from emerging to mature.

The event opened with a figure that has stuck with me. Only around 3-4% of nature assets are currently insured. In property markets, insurance is near-universal. Nobody buys a house on promises alone, without insuring what they are acquiring. Yet in nature markets, where we are asking billions in capital to flow into long-term, complex projects, this absence of insurance has become the working assumption.

That is not because investors and developers have been reckless. For a long time, the conditions required for insurance to be practical simply were not in place, so a whole infrastructure of alternative tools emerged instead: buffer pools, ratings agencies, verification bodies. These made sense for their time and they have genuine value. But as the market evolves, there is a real case for going back to first principles and asking whether we can now start to use instruments that give real confidence in transactions, in the way mainstream markets do.

Whether a sector can be insured (and on what terms) is itself a signal of how mature it is.

A market asking for trust it has not fully earned

In property, insurance is simply assumed. You do not debate whether to insure a building you own. And if a home for sale turns out to be difficult to insure, because of subsidence, flood risk or structural problems, that is a serious red flag that affects the price and often reduces the seller's ability to shift it. In nature markets, that clear indicator is not there yet, and everything is a bit more ambiguous, a bit more 'bazaar'.

The people who have committed capital to nature markets in spite of this deserve more credit than they usually get. These are investors, developers and project teams who moved before the market was regulated and the risk well understood. Capital that flows into uncertain territory is not naive; it is what every emerging market needs to get off the ground. Without it, there is no sector to mature, and the ambiguity itself is a feature of where the market is.

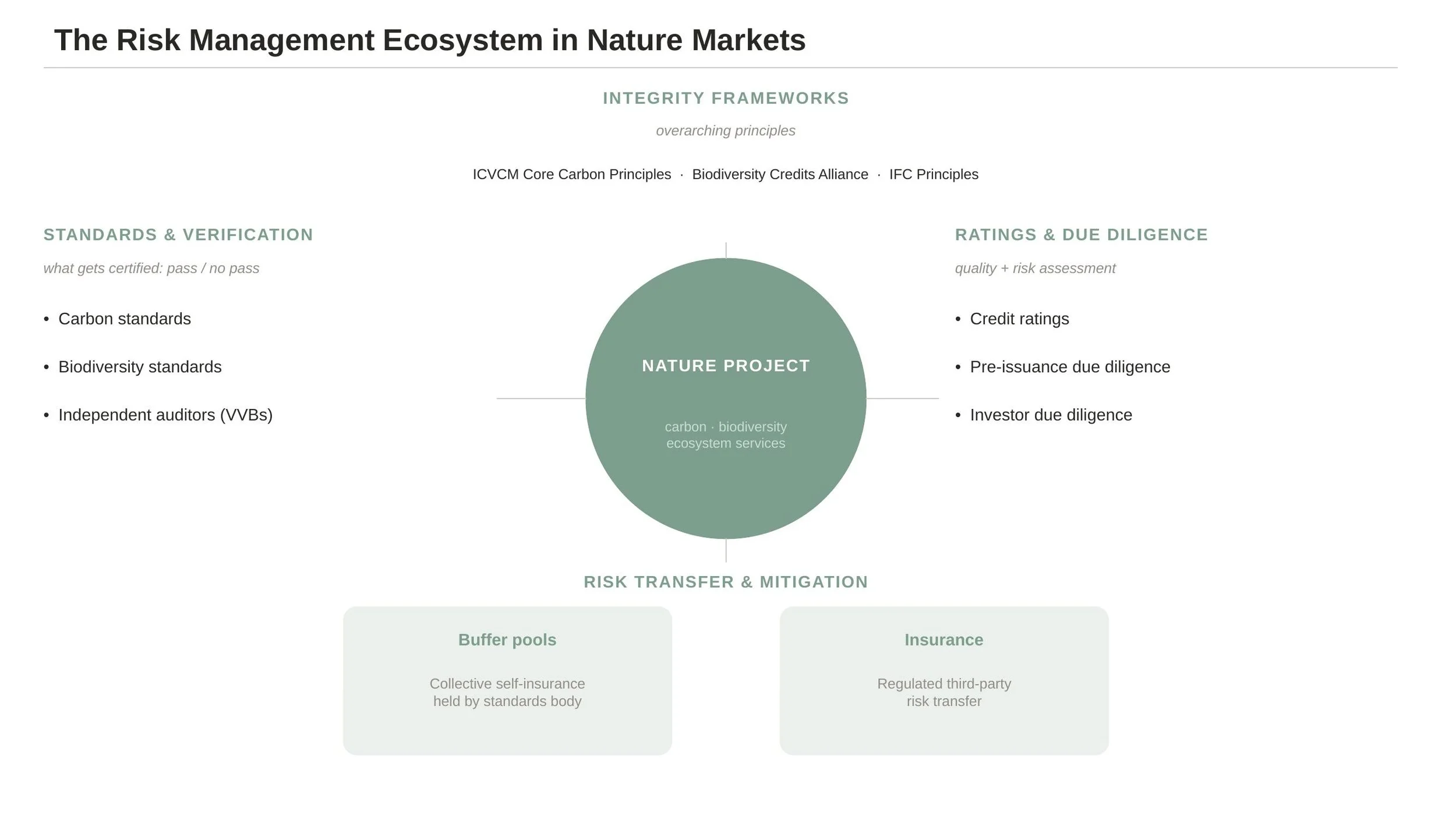

Without the structure and regulation of a mature market, the sector had to build its own basis for confidence as it went, and it did. Since 2021, the ecosystem of tools, frameworks and service providers to assess and manage risk expanded quickly. Carbon standards raised their benchmarks, ratings agencies grew in importance and sophistication, and due diligence platforms multiplied. Buffer pools, held by certification bodies, continued absorbing credit losses after verification. Some of this was a genuine and necessary response to a real gap. Some of it was more opportunistic: the sector clearly represented an opening, and a wave of new entrants moved in to offer de-risking tools of every shape and kind. Whether the market needed all of them is another question, and in any case, none of it was designed as a coherent system. Taken together, it raised the quality of the market, though only up to a point. Money still does not flow into nature restoration and conservation to the extent anyone had hoped.

Buffer pools are a good example of what improvised solutions can and cannot do. They work like a collective self-insurance mechanism, where projects contribute a percentage of their verified credits to a shared pool that absorbs losses against those units. Verified is the key word: buffer pools only protect against post-issuance reversal, meaning things going wrong after credits have already been issued and sold. They do not cover risks during development, before any units exist, and even within their intended scope they carry structural problems: the weakest link issue, where one underperforming project draws down the pool for everyone; solvency questions under correlated or catastrophic loss; and limited transparency for buyers about how deep the protection actually goes.

Ratings agencies emerged to answer a related problem from a different angle. In property, before you complete on a purchase, you commission a surveyor's report, an independent assessment of what you are actually buying. Carbon credit ratings serve a similar function: an external view of how likely a project is to deliver what it promises, before a buyer commits. Where buffer pools cover what happens after the fact, a rating is supposed to help buyers avoid bad decisions in the first place. Independent analysts have noted that the same project can receive meaningfully different scores from different rating agencies with no clear explanation why, which suggests the methodology is not always as solid as the market needs it to be.

The property parallel remains instructive here. A surveyor's report and buildings insurance do different jobs at different stages, where one tells you what you are buying and the other protects you once you own it. They are not alternatives but sequential steps, and the same logic applies in nature markets, where insurance does not replace a rating but covers a different moment in the risk timeline. What the example of one practitioner at the forum illustrated is that for some projects, at some scales, insurance covers enough ground that a separate rating adds little proportionate value, and that is not insurance winning so much as the market figuring out what it actually needs at different stages of maturity.

As insurance becomes more established, it is bound to reshape this improvised ecosystem and may, over time, become the most durable credibility anchor the sector has. Insurance involves regulated, capitalised third parties with real skin in the game, which is a different quality of commitment than most of what was built in the rush. Some of the tools that emerged will prove durable, and some will not. Offerings that were solving a problem that no longer exists in the same form will find their market shrinking, and some of those companies will fold. That is how markets mature, and the question for people and organisations who built these tools is whether they are thinking ahead about where they sit when the market no longer needs to improvise.

Insurance does not replace buffers; it can sit behind them, providing a creditworthy backstop that a self-managed pool cannot offer. Some emerging carbon standards are reportedly exploring whether insurance could directly backstop their buffer pools, which is a development worth keeping an eye on.

My own personal and non-expert mindmap for services and tools for risk management in nature management.

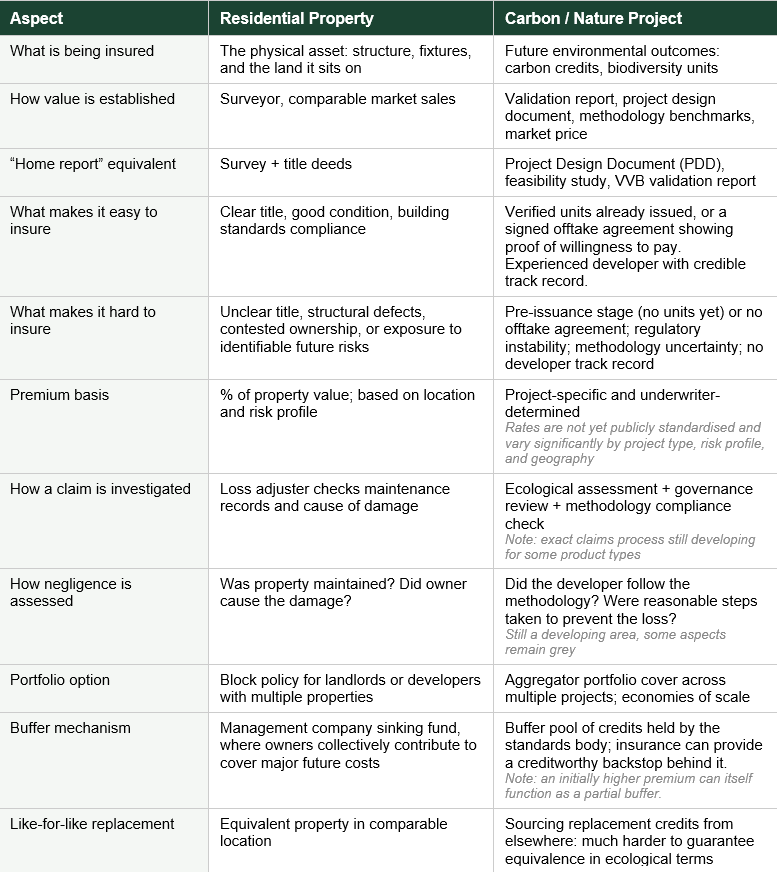

Nature projects and property: a practical comparison

The property analogy is not just rhetorical; you insure the nature on site as the asset, just as you insure the building. Think of it this way: you put in an offer on a house and get nervous, because your entire decision rests on a home report. It looks at the structure of the house based on what the surveyor can see from the outside and based on documentation from the seller, but it does not really look under the bonnet and cannot fully validate the current condition or flag imminent risks. You close, you own it, and then the boiler fails. Nobody covered that. In property markets, insurance fills exactly that gap; it means someone with real skin in the game has assessed the downside and put a price on it.

I met a good friend of mine in the pub last Friday. She looked stressed. She had bought a flat recently and six months in is faced with an ongoing dispute with a neighbour over a leaking pipe that seems to have no resolution, an issue that may well have been known to the previous owners. In her despair and exhaustion, she declared that she no longer wants to be an adult. Her flat probably had buildings insurance. It still did not spare her the dispute, the exhaustion, or the feeling that she had bought something she did not fully understand. Insurance is not a promise of smooth sailing; it is a measure of confidence from someone who has assessed the risk and put a price on the downside. Nature markets have been making do without that.

What makes nature assets harder to insure than buildings is largely a question of definition and clarity. The more clearly you can define what you have, what you are committed to delivering and what the willingness to pay for your credits is, the more you can insure against.

The table below is a clunky attempt at comparing nature projects to property. It is imperfect, nature assets do not behave like buildings and I am approaching this from a non-expert point of view, but I found it useful as a starting structure and would expect practitioners on either side to refine it.

Premium costs are project-specific and not yet publicly standardised. The commercial case for insurance generally holds when the cost per credit is lower than the price premium insured credits can command — but this varies by project.

What insurance products actually exist for Natural Capital projects

The nature insurance market is further along than most people realise, but it is not a concept that is as widely discussed as, let’s say, additionality. Many actors in the nature markets supply chain - developers, possibly even some people on the demand side, and definitely me - still struggle with getting a total grasp of the logistics and positining of insurance for Natural Capital. The categories of insurance products outline below is taken from a presentation by William Buttler of insurance broker Gaia Secura and representatives. It is a simplification and insuring a nature restoration project, for example, most likely requires a combination of insurance products, and modifications of each product.

• Restoration insurance covers the cost of restoring a project after a loss event, whether fire, disease, or natural occurrence, so the project can continue generating the credits it committed to.

• Replacement insurance covers the cost of sourcing equivalent credits elsewhere when restoration is not viable. This is the more complex product, and raises hard questions about what like-for-like means in ecological terms.

• Non-payment insurance protects developers and investors against default on offtake agreements or loan repayments. Standard cover can run to significant sums.

• General liability covers third-party claims arising from project operations.

In addition, as a representative of insurance provider Kita points out, political risk insurance covers regulatory change, government interference, and policy shifts in project jurisdictions. For anyone working in emerging markets, this one matters more than it is usually acknowledged. A contested or unstable regulatory framework can raise premiums significantly or make a project uninsurable. This is not a theoretical risk.

A real market signal that there is increasing uptake for carbon and nature markets insurance is that Kita - one of the pioneers in this space and a Lloyd’s coverholder - expanded its underwriting capacity by 40% to £22.5m in 2025. DUAL UK launched a biodiversity net gain insurance product in November 2025, extending the logic beyond carbon. Broker Gaia Sicura focuses specifically on natural capital risk transfer. These are early movers in a space that is still forming. I have linked sources at the end.

What makes a project insurable, and what does not

Underwriters need something to underwrite against. In practical terms that means a validated project, a clear legal framework for the units being generated, an experienced developer with a credible track record, an offtake agreement, and overall solid data. Insurance works best as a wrapper for existing contracts. When those elements are in place, the question of whether to insure becomes a commercial one rather than a practical barrier.

What makes a project hard to insure falls into two broad categories.

First, the absence of a contractual anchor: projects at the pre-issuance stage, or without an offtake agreement or sold credits, are difficult because there is no established value to work against. There is nothing to insure, in the same way you cannot insure a house that has not yet been built or valued. An asset doesn’t really have a clear value unless someone is willing to pay a certain amount for it.

Second, likely but hard-to-model future risks: regulatory instability, methodology changes, and limited developer track record all raise the question of what underwriters can reliably model. If the policy environment around carbon credits is contested or unclear, underwriters cannot price the risk. If a standards body updates its methodology and a project delivers fewer credits than projected, that is a loss even if the developer did everything right. These risks need to be addressed in project structure from the start, not retrofitted later. Remember, insurers don’t have to insure a project, it has to be feasible for them.

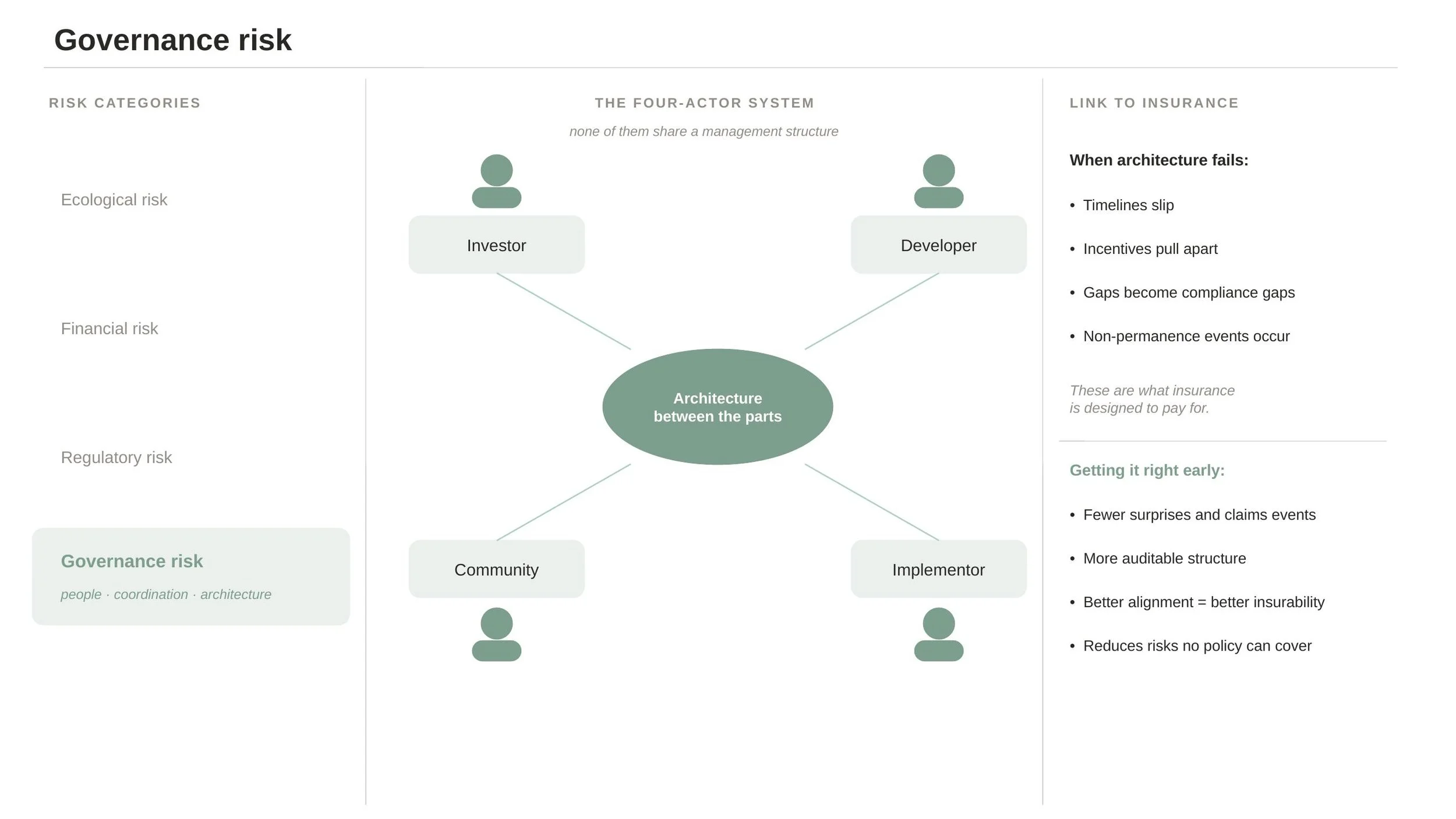

The people risk

Insurers, like certification bodies and ratings agencies before them, will need to assess risk across the standard categories used in nature project due diligence: ecological risks, financial risks, regulatory risks, governance risks. What I have picked up at a number of investor pitching events and forums is that governance and people elements kept coming up as the most uncertain and hardest to assess. Investors in NbS projects increasingly focus on the relationships between developers and implementors and the robustness of their processes. Management capacity and governance is a key pillar of any due diligence, but in particular within newer configurations of investor, project developer and implementor - especially with geographically dispersed teams - the enquiries need to go deeper, touching on the actual quality of internal communication flow and alignment. Key players in nature finance consistently raise the lack of a common language and information asymmetry as a significant issue, and it plays out between stakeholders at project level too. That caught my attention, because it is where most of my work sits.

Governance and management risk is already part of most assessment frameworks, aligned with the due diligence approaches used by investors, certifiers and ratings agencies alike. Underwriters typically look at developer track record, quality of project design, and reliability of implementing partners - all necessary, but focused on the pieces of the system rather than on the coordination and connectivity between them.

And that gap matters. In most nature projects, you have investors, developers, implementing organisations, and communities on the ground, none of whom share a management structure. They often operate with completely different professional cultures and incentives, yet are expected to function as a coherent system. Often, they do not.

I have worked in situations where the carbon and community workstreams were running in parallel, completely uncoordinated. Where the investor and developer had never stress-tested their assumptions about risk allocation with each other. Where the implementing team had no working understanding of what carbon compliance would actually require of them. The project was exposed in ways no insurance policy could cover. The risk was real. It just did not appear on any form.

The Verra risk register does ask about reliance on external partners, but it does not go far enough on this. And insurers, while they assess developer and implementor track records, are not yet systematically asking about the quality of the organisational architecture that holds these actors together.

My focus is that connectivity layer: the governance structures, information flows, and working relationships between investor, developer, implementor and community that nobody centrally manages but everyone depends on.

When this layer is not properly designed, the consequences are tangible. Delivery timelines slip, key delivery personnel can disengage, resource allocation gets misaligned, expectations are not met. Incentives that should reinforce each other start pulling in different directions. In the most serious cases, projects fail to deliver or lose permanence. This is not soft risk. Delays and a lack of alignment show up in investor returns, in community relations, and in the very non-permanence events that insurance policies are designed to cover. Getting this architecture right requires close attention from investors and developers who are willing to make it a priority from the start. The upside is direct: fewer surprises, less remediation, and a more resilient project. The operational reality either holds up against the promises made upstream, or it does not. That is usually a people problem before it is a methodology problem.

I keep wondering, though…

I should say upfront: I am not a specialist in insurance markets and I am aware of the limits of what I know here. But I do know how to ask questions. These are the ones that stayed with me after the forum. Do you have answers? Or further questions of your own?

• How does the service ecosystem shift as insurance grows? This is the question I find most interesting, and I am genuinely not sure of the answer. Ratings agencies, verification bodies, due diligence providers, buffer pools — all of these emerged to fill the trust gap in a market that did not yet have regulated risk transfer. As insurance develops, does the rest of the ecosystem evolve alongside it, or does the consolidation you see in maturing markets start to reshape who does what? My instinct is that insurance restructures the relationships rather than replacing the tools. Insurers need data to price risk, which creates a pull toward standardised inputs — this could commoditise some DD and ratings work, or push ratings agencies to compete on granularity rather than scale. Standards bodies may end up functioning more like building regulators: the framework within which insurance operates, rather than the primary quality signal. Buffer pools, which were always an imperfect workaround, may be repositioned as first-loss mechanisms sitting in front of insurance rather than serving as the main backstop. But this is speculation. I would be genuinely interested to know whether people currently providing these services are thinking ahead about where they sit in a more mature market.

• Will insurance access be more equitable than finance access? Smaller, community-led projects already struggle to get capital. The same legibility problem that blocks finance blocks insurance too. Hannah Rudman of Highland Rewilding raised this directly at the forum, and it deserves a direct answer rather than a footnote.

• Who is responsible for explaining to communities how risk and liability are allocated in the consortia they are part of? At what stage does that conversation happen, and who owns it? I have not seen this done consistently well yet.

• Risk transfer: who actually holds the risk in these structures, and how are they compensated for it? Is there transparency on where the risk ends up, and how it is being considered in financial models? For investors and developers building long-term structures, this feels like a question that needs a clearer answer than the market currently provides.

Sources

Kita — capacity expansion announcement (Apr 2025): https://www.kita.earth/blog/kita-expands-capacity-responding-to-growing-global-demand-for-carbon-insurance-solutions

DUAL — biodiversity net gain insurance launch: https://www.reinsurancene.ws/dual-to-support-biodiversity-net-gain-with-new-insurance-product/

CarbonPool — why carbon markets need a new approach to permanence: https://www.carbonpool.earth/buffer-pools-why-the-carbon-market-needs-a-new-approach-to-permanence-and-how-insurance-can-help/

Oka — shortcomings of the buffer pool as risk-mitigation mechanism: https://carboninsurance.co/the-shortcomings-of-the-buffer-pool-as-a-risk-mitigation-mechanism/

Sylvera — guide to carbon credit buffer pools: https://www.sylvera.com/blog/carbon-credit-buffer-pools

About the author

I work with organisations in nature finance on the layer that connects investors, developers, and implementing teams on the ground. My focus is on the people systems, governance structures, and stakeholder alignment that determine whether a nature project functions as designed, and whether the operational reality holds up against the promises made upstream. This is also the layer that most underwriting models do not yet reach. If you are working on a project or investment where stakeholder coherence is a challenge, or want to think through governance risk before it becomes a problem, I would be happy to talk.